Utang here, utang there… parang hindi na matapos-tapos. Tipong hindi ka pa nakakahinga sa isa, may naniningil na ulit. If you feel like you’re just working to pay bills and loan apps every month, take a deep breath. Hindi ka nag-iisa.

Many Filipinos are in the same boat—living paycheck to paycheck, juggling credit card bills, loan apps, tuition, and even those dreaded 5-6 loans. Minsan nakakahiya, minsan nakakalito, pero ang totoo: walang itinuturo sa atin kung paano talaga humawak ng pera at utang. Kaya ngayon, pag-uusapan natin kung paano makakaahon sa utang gamit ang isang simple pero powerful na tool: ang Debt Management Plan or DMP.

So ano nga ba ang Debt Management Plan?

A Debt Management Plan is a step-by-step strategy to help you organize your debts, create a realistic budget plan, and pay off what you owe without feeling overwhelmed. Hindi ito instant magic na mawawala bigla ang utang mo, pero it gives you control, clarity, and confidence na kaya mong lampasan ‘to.

In this blog, I’ll walk you through how to create your own personalized debt management plan Philippines style—yung swak sa income mo, lifestyle mo, at mga goals mo. Walang judgement, walang complicated jargon. Just clear, practical steps on how to get out of debt in the Philippines and rebuild your finances one payment at a time.

Kaya tara, simulan na natin ang journey mo to freedom.

What is a Debt Management Plan?

Let’s break it down, ano nga ba talaga ang Debt Management Plan o DMP? A Debt Management Plan (or DMP) is not a loan. Yes, you read that right—hindi ito dagdag na utang. Instead, it’s a structured repayment plan na tutulong sa’yo bayaran ang existing debts mo in a more manageable, organized way. Para itong game plan para unti-unting tapusin ang utang mo—isang buwan, isang bayad, isang hakbang sa pagbangon.

Think of it as your personalized “get out of debt” roadmap. Kung sa dami ng pinagkakautangan mo eh hindi mo na alam sino uunahin o paano ka magsisimula, a debt management plan Philippines-style can simplify all that. It helps you track what you owe, prioritize who to pay first, and create a budget plan that works for your current income. Bonus: minsan, it even helps you negotiate for lower monthly payments or waived penalties with your lenders. Mas gumagaan ang pasan.

Sino ang pwedeng gumamit ng DMP?

Well, kung ikaw ay may:

- Credit card debt na hindi na nababayaran in full

- Loan apps na halos kalahati ng sweldo mo ang kinukuha

- Past due bills na pinapatungan na ng interest

- O kahit yung na-stuck sa utang dahil emergency, layoff, o biglaang gastos

Then, you definitely need a debt management plan.

Ang mga benefits nito?

- Organized payment structure – Hindi mo na kailangan manghula kung sino ang susunod mong babayaran.

- Possible lower monthly payments – So hindi na kaagad ubos ang sweldo.

- Peace of mind – Kasi may plano ka na. Hindi man instant, pero sure ka sa direction.

Bottom line? A DMP won’t erase your debt overnight, pero it gives you the power to face it head-on—with a plan, with confidence, and with a clear path to freedom. Let’s keep going. Kayang-kaya mo ‘to.

Signs You Need a Debt Management Plan

Alam mo ‘yung feeling na kahit kakatanggap mo lang ng sweldo, ubos na agad? O yung tipong utang ang pinambabayad mo sa ibang utang? Kung oo, baka ito na ang sign mo, friend. Baka panahon na para gumawa ka ng Debt Management Plan—yung solid na strategy para makaahon sa utang at makontrol ulit ang finances mo.

Here are some warning signs na baka kailangan mo na talaga ng debt management plan Philippines style:

1. Utang ang Pangbayad sa Ibang Utang

A.K.A.. the classic “robbing Peter to pay Paul” situation.

Ginagamit mo na ang credit card mo para bayaran yung loan app? Or umutang ka kay officemate para pambayad sa credit card? That’s a big red flag. Hindi sustainable ‘yan, and eventually, mauubusan ka ng mapagkukuhanan. A DMP can help you organize all these debts para hindi ka na pa-ikot-ikot sa cycle na ‘to.

2. Maxed Out na ang Credit Card o Loan Apps

Kung halos wala ka nang ma-swipe sa credit card mo at puro “Past Due” na notification sa loan apps mo—that’s also a sign. Kapag na-max out mo na ang credit limit mo, ibig sabihin ubos na ang flexibility mo. A budget plan tied into a DMP can help you stop the bleeding and start clearing out these balances.

3. Naaanxiety ka na Tuwing May Tumatawag o Nagte-text

Let’s be real. Hindi lang pera ang nawawala kapag baon ka sa utang—pati peace of mind. Kung bawat text or tawag ay nagpapakaba sa’yo dahil baka collector na naman ‘yan, hindi mo na dapat palampasin. Debt affects your mental and emotional health. One huge benefit of a debt management plan is regaining control, so you don’t live in fear anymore.

4. ‘Di Mo Na Alam Saan Napupunta ang Sweldo Mo

“Parang may trabaho naman ako… pero bakit wala akong naiipon?”

If this sounds familiar, chances are hindi mo fully natatrack ang gastos mo. A DMP forces you to see the full picture—income, fixed expenses, variable spending, and all your debts—so you can build a realistic budget plan. The point is this: If one (or more) of these signs feels too close to home, huwag mong isipin na failure ka. Hindi ka nag-iisa. The good news? There’s a way out. A structured, step-by-step debt management plan can help you finally take control and start moving forward—one payment, one win, one brave decision at a time.

Step-by-Step: How to Create Your Own Debt Management Plan in the Philippines

Ready ka na ba? Dito na magsisimula ang tunay na pag-ahon. Ang goal natin? Gumawa ng solid na debt management plan Philippines-style na swak sa sitwasyon mo—simple, doable, at unti-unting magpapagaan ng load mo.

Here’s a step-by-step guide to help you build your own budget plan and finally get out of debt in the Philippines:

Step 1: List All Your Debts

Unang hakbang—aminin at ilista ang lahat ng utang. Kahit gaano pa yan kaliit o kalaki, isama mo. Walang skip, walang lihim.

Maaari kang gumamit ng notebook or, mas maganda, isang Google Sheet para makita mo lahat in one view. For each utang, isulat ang:

- Pangalan ng lender (e.g., SAFC, Home Credit, GCash, kay Ate Tess)

- Total amount due

- Interest rate (kung applicable)

- Monthly due date

Pro Tip: You can use a debt tracker template (you can download one or make your own). The goal here is clarity—para alam mo kung sino ang dapat unahin at magkano talaga ang kailangan mong bayaran monthly.

Step 2: Know Your Monthly Cash Flow

After mong makita ang lahat ng utang mo, next is to check kung gaano kalaki ang perang pumapasok at lumalabas kada buwan.

Sa madaling salita: Alamin mo ang cash flow mo.

- Total Monthly Income (lahat, kasama raket, allowance, side hustle)

- Total Fixed Expenses (renta, kuryente, tubig, internet, groceries)

- Variable Expenses (coffee, foodpanda, Shopee—aminin!)

Minsan, ‘di naman mahalaga ang laki ng income mo—mas importante kung paano mo siya hinahawakan.

Step 3: Prioritize & Categorize Your Debts

Ngayon na alam mo na kung gaano kalaki ang utang mo at gaano kalaki ang kinikita mo, let’s organize.

Paghiwalayin ang mga utang mo into:

- High Interest Debts – Usually mga loan apps or credit cards

- Low Interest Debts – Like SSS, Pag-IBIG, or salary deduction loans

- Urgent Debts – Yung may immediate deadline or risk (e.g., disconnection notice)

Then, decide what strategy to use:

- Debt Avalanche – Pay off the highest interest first. Makakatipid ka long-term.

- Debt Snowball – Pay off the smallest balance first. Mas mabilis ang motivation wins.

Pick one that suits your personality. Kung gusto mo makita agad ang progress, go for Snowball. Kung gusto mo makatipid sa interest, Avalanche is your best bet.

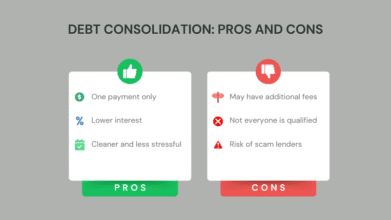

Step 4: Consolidate if Possible

If juggling multiple loans is too much, consider debt consolidation. This means combining all your debts into one loan with a lower monthly payment.

Pros:

- One payment only

- Lower interest (minsan)

- Cleaner and less stressful

Cons:

- May additional fees

- Not everyone is qualified

- Risk of scam lenders

Avoid 5-6 at mga too-good-to-be-true offers. Dumikit ka sa legit financial institutions like South Asialink Finance Corporation (SAFC) or trusted cooperatives na regulated by the BSP.

Step 5: Build a Bare-Bones Budget

Now that you know your debts and your cash flow, it’s time to build your budget plan.

This isn’t the time for YOLO spending. Focus muna sa needs over wants:

- ✅ Kuryente, tubig, pagkain

- ❌ Milk tea, Lazada haul

Try using the classic Sobre System (Envelope Budgeting). Maglagay ng cash sa labeled envelopes:

- Food

- Bills

- Debt

- Savings (kahit ₱100, okay na!)

Optional: Use our downloadable budget worksheet to keep things clean and visual.

Step 6: Automate & Track Your Progress

Set calendar reminders or use a simple app like Budget Planner by Spendee, Money Manager, or even just Google Calendar.

Every time you complete a payment, celebrate. Kahit maliit lang yan—₱500, ₱1,000—it’s progress!

Post it on your wall, write it in a journal, or treat yourself to a ₱20 taho. Ang mahalaga, you’re moving forward.

Final Reminder: Hindi mo kailangang gawin lahat ito in one day. Pero every step you take is a win. Bit by bit, bababa ang utang mo. And one day, you’ll look back and say, “Buti na lang nagsimula ako.”

Tuloy lang. This plan is for you.

Final Thoughts

Kung nabasa mo na lahat mula umpisa hanggang dito—grabe, solid ka. Ibig sabihin, gusto mo talagang ayusin ang sitwasyon mo. And let me tell you this: being in debt doesn’t mean failure. Hindi ka tamad. Hindi ka mahina. Hindi ka pabaya. Minsan, life just happens—biglaang gastos, family emergencies, nawalan ng trabaho, o minsan honest mistake lang talaga. And that’s okay.

Ang mahalaga ngayon? Gusto mong bumawi.

Creating a debt management plan Philippines-style isn’t just about numbers or spreadsheets—it’s about reclaiming your peace of mind, confidence, and future. Walang shortcut, pero merong direction. Hindi instant, pero sure kang may pupuntahan.

And remember: you don’t have to fix everything in one day.

Start small.

- List your utang.

- Track your gastos.

- Set a ₱500 goal for next payday.

Baby steps, pero forward steps.

Think of this journey as a reset. Hindi para i-punish ka, pero para bigyan ka ng second chance sa mas magaan, mas maayos, at mas empowered na version ng sarili mo. Your finances don’t define your worth—but how you handle them can shape your future.

Basta may plano ka. May effort ka. May mindset ka na “Ayoko nang manatili sa ganitong cycle.” That alone makes you powerful. Let this be the start of your comeback story.